This is a book summary of The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel.

I couldn’t ignore The Psychology of Money any longer. It seems like everyone is talking about it in my little corner of Twitter. Many are calling it their top book of the year.

And, Amazon supports the hype. The book launched in September 2020 and already has over 2,500 ratings.

If you’re looking for an intro to Morgan Housel, here you go:

Quick Housekeeping:

- All quotes are from the author, Morgan Housel, unless otherwise stated.

- I’ve added my own emphasis in bold.

Book Summary Contents: Click a link here to jump to a section below

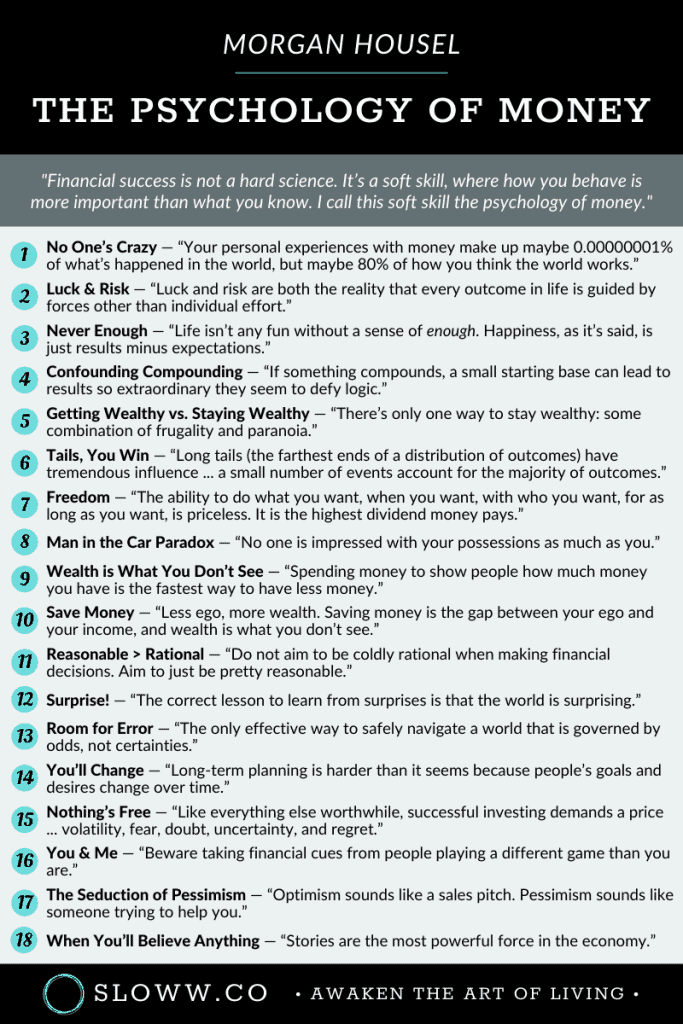

- No One’s Crazy

- Luck & Risk

- Never Enough

- Confounding Compounding

- Getting Wealthy vs. Staying Wealthy

- Tails, You Win

- Freedom

- Man in the Car Paradox

- Wealth is What You Don’t See

- Save Money

- Reasonable > Rational

- Surprise!

- Room for Error

- You’ll Change

- Nothing’s Free

- You & Me

- The Seduction of Pessimism

- When You’ll Believe Anything

18 Wealth Lessons from “The Psychology of Money” by Morgan Housel (Book Summary)

Overview of The Psychology of Money:

“The premise of this book is that doing well with money has a little to do with how smart you are and a lot to do with how you behave.”

- “Financial success is not a hard science. It’s a soft skill, where how you behave is more important than what you know. I call this soft skill the psychology of money.”

- “The aim of this book is to use short stories to convince you that soft skills are more important than the technical side of money.”

- “We think about and are taught about money in ways that are too much like physics (with rules and laws) and not enough like psychology (with emotions and nuance).”

- “Physics isn’t controversial. It’s guided by laws. Finance is different. It’s guided by people’s behaviors.“

1. No One’s Crazy

“Your personal experiences with money make up maybe 0.00000001% of what’s happened in the world, but maybe 80% of how you think the world works.”

- “Every decision people make with money is justified by taking the information they have at the moment and plugging it into their unique mental model of how the world works.”

- “People do some crazy things with money. But no one is crazy. Here’s the thing: People from different generations, raised by different parents who earned different incomes and held different values, in different parts of the world, born into different economies, experiencing different job markets with different incentives and different degrees of luck, learn very different lessons.”

- “In theory people should make investment decisions based on their goals and the characteristics of the investment options available to them at the time. But that’s not what people do. The economists found that people’s lifetime investment decisions are heavily anchored to the experiences those investors had in their own generation—especially experiences early in their adult life.”

- “Their view of money was formed in different worlds. And when that’s the case, a view about money that one group of people thinks is outrageous can make perfect sense to another.”

- “Few people make financial decisions purely with a spreadsheet. They make them at the dinner table, or in a company meeting. Places where personal history, your own unique view of the world, ego, pride, marketing, and odd incentives are scrambled together into a narrative that works for you.”

2. Luck & Risk

“Luck and risk are both the reality that every outcome in life is guided by forces other than individual effort. They are so similar that you can’t believe in one without equally respecting the other. They both happen because the world is too complex to allow 100% of your actions to dictate 100% of your outcomes.”

- “They are driven by the same thing: You are one person in a game with seven billion other people and infinite moving parts. The accidental impact of actions outside of your control can be more consequential than the ones you consciously take.“

- “The line between ‘inspiringly bold’ and ‘foolishly reckless’ can be a millimeter thick and only visible with hindsight. Risk and luck are doppelgangers.”

- “Be careful who you praise and admire. Be careful who you look down upon and wish to avoid becoming. Or, just be careful when assuming that 100% of outcomes can be attributed to effort and decisions.”

- “Therefore, focus less on specific individuals and case studies and more on broad patterns.”

- “Go out of your way to find humility when things are going right and forgiveness / compassion when they go wrong. Because it’s never as good or as bad as it looks.“

- “You should like risk because it pays off over time. But you should be paranoid of ruinous risk because it prevents you from taking future risks that will pay off over time.”

3. Never Enough

“Life isn’t any fun without a sense of enough. Happiness, as it’s said, is just results minus expectations.”

- “‘Enough’ is not too little … ‘Enough’ is realizing that the opposite—an insatiable appetite for more—will push you to the point of regret.”

- “The hardest financial skill is getting the goalpost to stop moving. But it’s one of the most important. If expectations rise with results there is no logic in striving for more because you’ll feel the same after putting in extra effort. It gets dangerous when the taste of having more—more money, more power, more prestige—increases ambition faster than satisfaction.”

- “Social comparison is the problem here … The point is that the ceiling of social comparison is so high that virtually no one will ever hit it. Which means it’s a battle that can never be won, or that the only way to win is to not fight to begin with—to accept that you might have enough, even if it’s less than those around you.”

- “There is no reason to risk what you have and need for what you don’t have and don’t need.”

- “There are many things never worth risking, no matter the potential gain.”

- “Maintaining a lifestyle below what you can afford is avoiding the psychological treadmill of keeping up with the Joneses.” (Note: See voluntary simplicity)

4. Confounding Compounding

“If something compounds—if a little growth serves as the fuel for future growth—a small starting base can lead to results so extraordinary they seem to defy logic. It can be so logic-defying that you underestimate what’s possible, where growth comes from, and what it can lead to.”

- “$81.5 billion of Warren Buffett’s $84.5 billion net worth came after his 65th birthday. Our minds are not built to handle such absurdities.”

- “His skill is investing, but his secret is time. That’s how compounding works.”

- “If you want to do better as an investor, the single most powerful thing you can do is increase your time horizon. Time is the most powerful force in investing.”

- “Good investing isn’t necessarily about earning the highest returns, because the highest returns tend to be one-off hits that can’t be repeated. It’s about earning pretty good returns that you can stick with and which can be repeated for the longest period of time. That’s when compounding runs wild.”

5. Getting Wealthy vs. Staying Wealthy

“There are a million ways to get wealthy … but there’s only one way to stay wealthy: some combination of frugality and paranoia.”

- “Good investing is not necessarily about making good decisions. It’s about consistently not screwing up.“

- “If I had to summarize money success in a single word it would be ‘survival.'”

- “Getting money requires taking risks, being optimistic, and putting yourself out there. But keeping money requires the opposite of taking risk. It requires humility, and fear that what you’ve made can be taken away from you just as fast. It requires frugality and an acceptance that at least some of what you’ve made is attributable to luck, so past success can’t be relied upon to repeat indefinitely.”

- “The ability to stick around for a long time, without wiping out or being forced to give up, is what makes the biggest difference. This should be the cornerstone of your strategy, whether it’s in investing or your career or a business you own. There are two reasons why a survival mentality is so key with money. One is the obvious: few gains are so great that they’re worth wiping yourself out over. The other is the counterintuitive math of compounding. Compounding only works if you can give an asset years and years to grow.”

- “More than I want big returns, I want to be financially unbreakable. And if I’m unbreakable I actually think I’ll get the biggest returns, because I’ll be able to stick around long enough for compounding to work wonders.”

- “Planning is important, but the most important part of every plan is to plan on the plan not going according to plan … Many bets fail not because they were wrong, but because they were mostly right in a situation that required things to be exactly right. Room for error—often called margin of safety—is one of the most underappreciated forces in finance. It comes in many forms: A frugal budget, flexible thinking, and a loose timeline—anything that lets you live happily with a range of outcomes.”

- “A barbelled personality—optimistic about the future, but paranoid about what will prevent you from getting to the future—is vital.”

6. Tails, You Win

“A lot of things in business and investing work this way. Long tails—the farthest ends of a distribution of outcomes—have tremendous influence in finance, where a small number of events can account for the majority of outcomes.“

- “That can be hard to deal with, even if you understand the math. It is not intuitive that an investor can be wrong half the time and still make a fortune. It means we underestimate how normal it is for a lot of things to fail. Which causes us to overreact when they do.”

- “Anything that is huge, profitable, famous, or influential is the result of a tail event—an outlying one-in-thousands or millions event. And most of our attention goes to things that are huge, profitable, famous, or influential. When most of what we pay attention to is the result of a tail, it’s easy to underestimate how rare and powerful they are.”

- “A good definition of an investing genius is the man or woman who can do the average thing when all those around them are going crazy. Tails drive everything.“

7. Freedom

“The ability to do what you want, when you want, with who you want, for as long as you want, is priceless. It is the highest dividend money pays.“

- “The highest form of wealth is the ability to wake up every morning and say, ‘I can do whatever I want today.’ People want to become wealthier to make them happier. Happiness is a complicated subject because everyone’s different. But if there’s a common denominator in happiness—a universal fuel of joy—it’s that people want to control their lives.”

- “More than your salary. More than the size of your house. More than the prestige of your job. Control over doing what you want, when you want to, with the people you want to, is the broadest lifestyle variable that makes people happy.“

- “Money’s greatest intrinsic value—and this can’t be overstated—is its ability to give you control over your time. To obtain, bit by bit, a level of independence and autonomy that comes from unspent assets that give you greater control over what you can do and when you can do it.”

- “Using your money to buy time and options has a lifestyle benefit few luxury goods can compete with.”

- “Aligning money towards a life that lets you do what you want, when you want, with who you want, where you want, for as long as you want, has incredible return.”

- “Being able to wake up one morning and change what you’re doing, on your own terms, whenever you’re ready, seems like the grandmother of all financial goals. Independence, to me, doesn’t mean you’ll stop working. It means you only do the work you like with people you like at the times you want for as long as you want.”

8. Man in the Car Paradox

“No one is impressed with your possessions as much as you are.”

- “There is a paradox here: people tend to want wealth to signal to others that they should be liked and admired. But in reality those other people often bypass admiring you, not because they don’t think wealth is admirable, but because they use your wealth as a benchmark for their own desire to be liked and admired.“

- “It’s a subtle recognition that people generally aspire to be respected and admired by others, and using money to buy fancy things may bring less of it than you imagine. If respect and admiration are your goal, be careful how you seek it. Humility, kindness, and empathy will bring you more respect than horsepower ever will.“

9. Wealth is What You Don’t See

“Spending money to show people how much money you have is the fastest way to have less money.”

- “We tend to judge wealth by what we see, because that’s the information we have in front of us. We can’t see people’s bank accounts or brokerage statements. So we rely on outward appearances to gauge financial success. Cars. Homes. Instagram photos. Modern capitalism makes helping people fake it until they make it a cherished industry.”

- “The truth is that wealth is what you don’t see. Wealth is the nice cars not purchased. The diamonds not bought. The watches not worn, the clothes forgone and the first-class upgrade declined. Wealth is financial assets that haven’t yet been converted into the stuff you see. That’s not how we think about wealth, because you can’t contextualize what you can’t see.”

- “The only way to be wealthy is to not spend the money that you do have. It’s not just the only way to accumulate wealth; it’s the very definition of wealth. We should be careful to define the difference between wealthy and rich. It is more than semantics. Not knowing the difference is a source of countless poor money decisions.”

- “Rich is a current income. Someone driving a $100,000 car is almost certainly rich, because even if they purchased the car with debt you need a certain level of income to afford the monthly payment. Same with those who live in big homes. It’s not hard to spot rich people. They often go out of their way to make themselves known.”

- “Wealth is hidden. It’s income not spent. Wealth is an option not yet taken to buy something later. Its value lies in offering you options, flexibility, and growth to one day purchase more stuff than you could right now.”

- “People are good at learning by imitation. But the hidden nature of wealth makes it hard to imitate others and learn from their ways.”

10. Save Money

“Building wealth has little to do with your income or investment returns, and lots to do with your savings rate.”

- “Independence, at any income level, is driven by your savings rate.” (Note: See FIRE (Financial Independence Retire Early))

- “Personal savings and frugality—finance’s conservation and efficiency—are parts of the money equation that are more in your control and have a 100% chance of being as effective in the future as they are today.”

- “Wealth is just the accumulated leftovers after you spend what you take in. And since you can build wealth without a high income, but have no chance of building wealth without a high savings rate, it’s clear which one matters more.”

- “Learning to be happy with less money creates a gap between what you have and what you want—similar to the gap you get from growing your paycheck, but easier and more in your control. A high savings rate means having lower expenses than you otherwise could, and having lower expenses means your savings go farther than they would if you spent more.”

- “Spending beyond a pretty low level of materialism is mostly a reflection of ego approaching income, a way to spend money to show people that you have (or had) money. Think of it like this, and one of the most powerful ways to increase your savings isn’t to raise your income. It’s to raise your humility. When you define savings as the gap between your ego and your income you realize why many people with decent incomes save so little.”

- “Savings can be created by spending less. You can spend less if you desire less. And you will desire less if you care less about what others think of you.”

- “You don’t need a specific reason to save … You can save just for saving’s sake. And indeed you should. Everyone should.”

- “Everyone knows the tangible stuff money buys. The intangible stuff is harder to wrap your head around, so it tends to go unnoticed. But the intangible benefits of money can be far more valuable and capable of increasing your happiness than the tangible things that are obvious targets of our savings. Savings without a spending goal gives you options and flexibility, the ability to wait and the opportunity to pounce. It gives you time to think. It lets you change course on your own terms.”

- “Savings in the bank that earn 0% interest might actually generate an extraordinary return if they give you the flexibility to take a job with a lower salary but more purpose, or wait for investment opportunities that come when those without flexibility turn desperate.”

- “If you have flexibility you can wait for good opportunities, both in your career and for your investments. You’ll have a better chance of being able to learn a new skill when it’s necessary. You’ll feel less urgency to chase competitors who can do things you can’t, and have more leeway to find your passion and your niche at your own pace. You can find a new routine, a slower pace, and think about life with a different set of assumptions.”

- “Having more control over your time and options is becoming one of the most valuable currencies in the world.”

- “Less ego, more wealth. Saving money is the gap between your ego and your income, and wealth is what you don’t see.”

11. Reasonable > Rational

“Do not aim to be coldly rational when making financial decisions. Aim to just be pretty reasonable. Reasonable is more realistic and you have a better chance of sticking with it for the long run, which is what matters most when managing money.”

- “What’s often overlooked in finance is that something can be technically true but contextually nonsense.”

- “A rational investor makes decisions based on numeric facts. A reasonable investor makes them in a conference room surrounded by co-workers you want to think highly of you, with a spouse you don’t want to let down, or judged against the silly but realistic competitors that are your brother-in-law, your neighbor, and your own personal doubts. Investing has a social component that’s often ignored when viewed through a strictly financial lens.“

12. Surprise!

“The correct lesson to learn from surprises is that the world is surprising. Not that we should use past surprises as a guide to future boundaries; that we should use past surprises as an admission that we have no idea what might happen next.”

- “History is the study of change, ironically used as a map of the future.”

- “It is smart to have a deep appreciation for economic and investing history. History helps us calibrate our expectations, study where people tend to go wrong, and offers a rough guide of what tends to work. But it is not, in any way, a map of the future.“

- “A trap many investors fall into is what I call ‘historians as prophets’ fallacy: An overreliance on past data as a signal to future conditions in a field where innovation and change are the lifeblood of progress.”

- “The most important driver of anything tied to money is the stories people tell themselves and the preferences they have for goods and services. Those things don’t tend to sit still. They change with culture and generation. They’re always changing and always will.”

- “The most important economic events of the future—things that will move the needle the most—are things that history gives us little to no guide about. They will be unprecedented events. Their unprecedented nature means we won’t be prepared for them, which is part of what makes them so impactful. This is true for both scary events like recessions and wars, and great events like innovation.”

- “History can be a misleading guide to the future of the economy and stock market because it doesn’t account for structural changes that are relevant to today’s world.”

- “The further back in history you look, the more general your takeaways should be. General things like people’s relationship to greed and fear, how they behave under stress, and how they respond to incentives tend to be stable in time. The history of money is useful for that kind of stuff. But specific trends, specific trades, specific sectors, specific causal relationships about markets, and what people should do with their money are always an example of evolution in progress. Historians are not prophets.”

13. Room for Error

“Margin of safety—you can also call it room for error or redundancy—is the only effective way to safely navigate a world that is governed by odds, not certainties. And almost everything related to money exists in that kind of world.”

- “Worship room for error. A gap between what could happen in the future and what you need to happen in the future in order to do well is what gives you endurance, and endurance is what makes compounding magic over time.”

- “The most important part of every plan is planning on your plan not going according to plan.”

- “There is never a moment when you’re so right that you can bet every chip in front of you. The world isn’t that kind to anyone—not consistently, anyways. You have to give yourself room for error. You have to plan on your plan not going according to plan.“

- “History is littered with good ideas taken too far, which are indistinguishable from bad ideas. The wisdom in having room for error is acknowledging that uncertainty, randomness, and chance—’unknowns’—are an ever-present part of life. The only way to deal with them is by increasing the gap between what you think will happen and what can happen while still leaving you capable of fighting another day.”

- “Two things cause us to avoid room for error. One is the idea that somebody must know what the future holds, driven by the uncomfortable feeling that comes from admitting the opposite. The second is that you’re therefore doing yourself harm by not taking actions that fully exploit an accurate view of that future coming true.”

- “If there’s one way to guard against their damage, it’s avoiding single points of failure. A good rule of thumb for a lot of things in life is that everything that can break will eventually break. So if many things rely on one thing working, and that thing breaks, you are counting the days to catastrophe. That’s a single point of failure.”

- “The biggest single point of failure with money is a sole reliance on a paycheck to fund short-term spending needs, with no savings to create a gap between what you think your expenses are and what they might be in the future.”

14. You’ll Change

“Long-term planning is harder than it seems because people’s goals and desires change over time.”

- “An underpinning of psychology is that people are poor forecasters of their future selves. Imagining a goal is easy and fun. Imagining a goal in the context of the realistic life stresses that grow with competitive pursuits is something entirely different. This has a big impact on our ability to plan for future financial goals.”

- “The End of History Illusion is what psychologists call the tendency for people to be keenly aware of how much they’ve changed in the past, but to underestimate how much their personalities, desires, and goals are likely to change in the future.”

- “We should avoid the extreme ends of financial planning. Assuming you’ll be happy with a very low income, or choosing to work endless hours in pursuit of a high one, increases the odds that you’ll one day find yourself at a point of regret.”

- “We should also come to accept the reality of changing our minds.”

15. Nothing’s Free

“Everything has a price, but not all prices appear on labels.”

- “Everything has a price, and the key to a lot of things with money is just figuring out what that price is and being willing to pay it. The problem is that the price of a lot of things is not obvious until you’ve experienced them firsthand, when the bill is overdue.”

- “Most things are harder in practice than they are in theory. Sometimes this is because we’re overconfident. More often it’s because we’re not good at identifying what the price of success is, which prevents us from being able to pay it.”

- “Like everything else worthwhile, successful investing demands a price. But its currency is not dollars and cents. It’s volatility, fear, doubt, uncertainty, and regret—all of which are easy to overlook until you’re dealing with them in real time.”

- “The question is: Why do so many people who are willing to pay the price of cars, houses, food, and vacations try so hard to avoid paying the price of good investment returns? The answer is simple: The price of investing success is not immediately obvious. It’s not a price tag you can see, so when the bill comes due it doesn’t feel like a fee for getting something good. It feels like a fine for doing something wrong. And while people are generally fine with paying fees, fines are supposed to be avoided. You’re supposed to make decisions that preempt and avoid fines.”

- “It sounds trivial, but thinking of market volatility as a fee rather than a fine is an important part of developing the kind of mindset that lets you stick around long enough for investing gains to work in your favor.”

- “Market returns are never free and never will be. They demand you pay a price, like any other product.”

- “The trick is convincing yourself that the market’s fee is worth it. That’s the only way to properly deal with volatility and uncertainty—not just putting up with it, but realizing that it’s an admission fee worth paying. There’s no guarantee that it will be.”

- “Define the cost of success and be ready to pay for it. Because nothing worthwhile is free.”

16. You & Me

“Beware taking financial cues from people playing a different game than you are.”

- “An idea exists in finance that seems innocent but has done incalculable damage. It’s the notion that assets have one rational price in a world where investors have different goals and time horizons.”

- “Bubbles form when the momentum of short-term returns attracts enough money that the makeup of investors shifts from mostly long term to mostly short term.”

- “The formation of bubbles isn’t so much about people irrationally participating in long-term investing. They’re about people somewhat rationally moving toward short-term trading to capture momentum that had been feeding on itself.“

- “It’s hard to grasp that other investors have different goals than we do, because an anchor of psychology is not realizing that rational people can see the world through a different lens than your own. Rising prices persuade all investors in ways the best marketers envy. They are a drug that can turn value-conscious investors into dewy-eyed optimists, detached from their own reality by the actions of someone playing a different game than they are.”

- “A takeaway here is that few things matter more with money than understanding your own time horizon and not being persuaded by the actions and behaviors of people playing different games than you are. The main thing I can recommend is going out of your way to identify what game you’re playing.”

- “Smart, informed, and reasonable people can disagree in finance, because people have vastly different goals and desires. There is no single right answer; just the answer that works for you.“

17. The Seduction of Pessimism

“Optimism sounds like a sales pitch. Pessimism sounds like someone trying to help you.”

- “Optimism is a belief that the odds of a good outcome are in your favor over time, even when there will be setbacks along the way.”

- “Money is ubiquitous, so something bad happening tends to affect everyone and captures everyone’s attention.”

- “Pessimists often extrapolate present trends without accounting for how markets adapt.”

- “Progress happens too slowly to notice, but setbacks happen too quickly to ignore.”

- “It’s easier to create a narrative around pessimism because the story pieces tend to be fresher and more recent. Optimistic narratives require looking at a long stretch of history and developments, which people tend to forget and take more effort to piece together.”

18. When You’ll Believe Anything

“Stories are, by far, the most powerful force in the economy. They are the fuel that can let the tangible parts of the economy work, or the brake that holds our capabilities back.”

- “The more you want something to be true, the more likely you are to believe a story that overestimates the odds of it being true.”

- “An appealing fiction happens when you are smart, you want to find solutions, but face a combination of limited control and high stakes. They are extremely powerful. They can make you believe just about anything.”

- “Incentives are a powerful motivator, and we should always remember how they influence our own financial goals and outlooks. It can’t be overstated: there is no greater force in finance than room for error, and the higher the stakes, the wider it should be.”

- “Everyone has an incomplete view of the world. But we form a complete narrative to fill in the gaps.”

- “Wanting to believe that we are in control is an emotional itch that needs to be scratched, rather than an analytical problem to be calculated and solved. The illusion of control is more persuasive than the reality of uncertainty. So we cling to stories about outcomes being in our control.“

You May Also Enjoy:

- Top book summaries (or browse all book summaries)